According to the recently released Swatch Group Half-Year 2017 Report, there was 6.8% to CHF 281 million net income increase for the 1st half of 2017 as compared to the same period in 2016 with CHF 263 million; confirming a Friday, 21 July Financial Times report of evidence for a rebound in Swiss watchmaking and a return to profits and sales growth for the first half of 2017.

Business of Luxury: Swiss Watch Industry Overview – Then and Now

Having been weaned on a diet of luxury watchmaking, the Swiss Watch Industry has grown to gargantuan proportions. It’s almost hard to imagine how in the year 2000, high end Swiss watches as defined by Swiss Customs/FH data – costing CHF 3000 and above were only 15.5% of 488,000 units in the industry.

In five years, they almost doubled, moving 731,000 units but accounted for 41.3% of total official Swiss watch export value. By 2014, the sums more than doubled, hitting 1,643,000 units to peak at 62% in 2014 and 2015.

In short, after close to two decades of exuberant (perhaps irrational growth), the Swiss watch industry with export values of CHF 3,153 million in 2000 versus CHF 13,415 million in 2015 was about to go on its first diet in 15 years. And boy, what a painful three year diet it has been.

The Swatch Group Half-Year report for 2017 confirms similar analysis from Bloomberg which posted positive recovery of the Swiss watch industry with export growth in June 2017 trending 5.3% higher than the same period in 2016.

Movement supply to the industry was dominantly provided by Swatch Groups ETA

With CHF 3,759 million Group net sales of +1.2% at constant exchange rates and +2.9% sales growth at constant rates in Watches & Jewellery segment excluding production (that is to say movement and component supply to external parties), Swatch Group’s Half Year report for 2017 ends a particularly bad 2016 with small but in context, critically important recovery.

Tellingly, despite negative currency impact resulting from a stronger than expected Swiss Franc as explained by Financial Times – continued weakness in the euro means the Swiss Franc builds on its Brexit-vote surge with the currency being at its strongest levels in 18 months, operating margins in the Watches & Jewellery segment excluding production increased by almost 25% from 10.7% to 13.2% versus the year before when inclusive of production, the segment only achieved 11.8%.

Outside of the Swatch Group 2017 Half-Year Report, Swiss Customs/FH data suggests that recovery is sustained in several markets: Italy is up 16.5% with a second month of strong growth. The United Kingdom enjoyed advantageous FOREX and is recording +35.6% growth, the strongest in more than two years. China continues its three month run of gains with 11.5% growth in a positive first half of 2017. The United States however, saw no change, declining slightly, -1.3% in June. Japan is still firmly in negative territory, sharply lower with -15.4%, oddly, they’re still buying Ferraris according to East Asia Hub CEO Dieter Knechtel.

The Group’s performance in those regions varied depending on local currency with Mainland China recording significant growth, stabilised sales in Hong Kong, a mixed picture in Japan and very positive sales in the Middle East with modest gains in the UK, Spain, Italy and Switzerland. The US was also in positive territory for the group in local currency but once accounted for the weak USD, there was no growth in CHF. Meanwhile, the 2017 Half-Year report also notes that sales to local consumers were positive, inverse to sales to Chinese tourists which decreased as a result of the negative currency situation.

Swatch Group stays the course – A recipe for success during turbulent times

When the market started to correct itself, Swatch Group Chief Executive Nick Hayek steadfastly refused to trim his workforce in stark contrast to competing watchmaking conglomerate Richemont Group which axed around 200 employees at Cartier, Piaget and Vacheron Constantin; it was a move similarly followed by other watchmaking outfits like Movado and Parmigiani. His rationale was that when the market recovered, Swatch Group would be in position to exploit the recovery of demand; thus long-term Group strategy was to keep its personnel employed despite lower sales in Production and to further invest in the production base.

“It may have meant we earned less for a while, but once volume comes back, we’ll earn more than average,” Hayek to Bloomberg

At the onset, the deliberate choice to retain jobs despite less than optimal capacity utilisation compared to the previous year resulted in temporarily lower operating margins. As of June 2017, the number of employees at the Group is approximately 35,000 with Swatch Group shares gaining as much as 2.4% in early Zurich trading on the news that the Group was able to respond quickly to the pickup in demand observed last Autumn. Hayek’s Group strategy mirrors a previous position during the last financial crisis in 2008 when he too refused to cut jobs.

Meanwhile, Richemont Group’s 2017 fiscal year ending March 31 reported that group sales were down to €10.7 billion, a 4% drop from the previous year with profits down close to 46% to €1.2 billion with biggest declines coming mainly from the watches segment of its watches and jewellery division, down 15% in contrast to jewellery which was up 7%. The Group’s other holdings in apparel brands which were down 6% with leather goods up 11% causing the group to pivot to Chloe as reported in Business of Fashion.

Swatch Group increased orders compared to the previous period with production of certain components, particularly watch cases ramped up. Also, integrated gold production from foundry to production of semi-finished goods was centralised in Swatch Group which led to synergies and optimised production flow contributing to the inverse relationship where the Group reported CHF 3,716 million in the 1st half of 2016 as opposed to CHF 3,705 million in the first half of 2017 yet allowing the Group enjoying better Operating results growing 5.1% to CHF 371 million in the first half of 2017 as opposed to CHF 353 in the same period last year, a seven-year low. Net income for Swatch Group’s first half 2017 was CHF 281 million.

Swatch Group’s bestsellers

- Speedy Tuesday 60th anniversary Omega Speedmaster was sold out online in 4 hours

- Good revenues with launch of Swatch New Skin, Swatch X You and Sistem51 Irony

- Longines did well with first editions of Longines Master Collection Blue

- Tissot Ballade Silicum and T-race Cycling generated high volumes

- Prestige and Luxury segment, new products accelerated growth in high double digits particularly Harry Winston high jewellery Lotus Cluster, Art Deco and Sunflower and the exclusive watch model – Midnight Date Moon Phase

- Breguet was especially successful with new ladies’ collection – Tradition and Phase de Lune

- Blancpain enjoyed gains with Villeret and Bathyscaphe collections

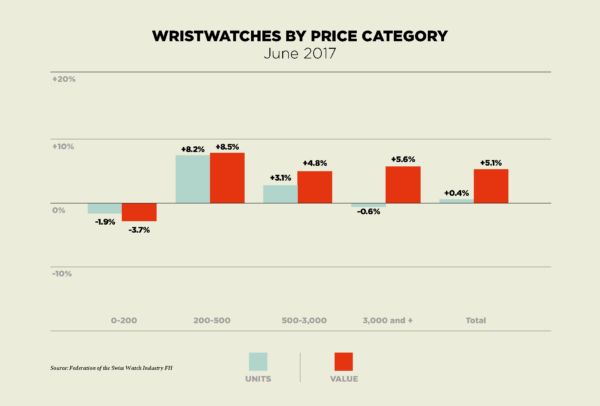

The stats reveal something interesting afoot in the Swiss Watch Industry

Sales of Swiss watches priced CHF200 and below are fairing poorly

Aside from the highest tiers of watchmaking, something interesting is afoot in the industry, sales of CHF200 watches have not only not recovered but have actually gone down while other more expensive watches have grown, especially in the CHF200 to 500 range. The lower end segment is likely more threatened by tech wearables like fitbits, smart watches and of course, the interesting Scandinavian and Norwegian brands like Skaagen and Triwa. We are probably about to witness a consolidation of that sector very soon.